Every Tuesday afternoon we publish a collection of topics and give our expert opinion about the Equity Markets.

The RBA board return from their holidays today to discuss interest rate policy for Australia and this has the pundits wagging their tongues prophesying the result. ABSI this week analyses the various outcomes on where interest rates in Australia are heading.

Key Economic Data

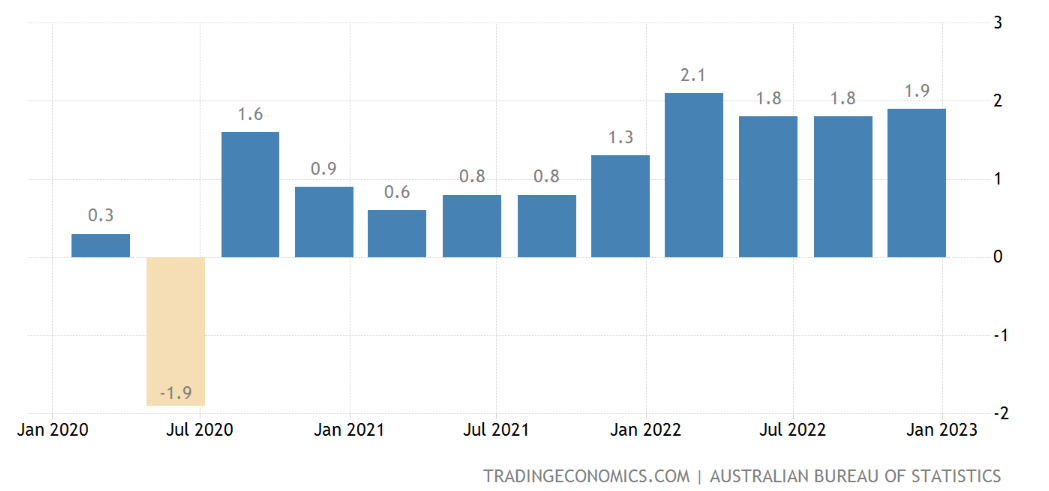

It is important to appreciate the critical data points that have been released recently which will weigh on the minds of the RBA board. Paramount was Q4 2022 inflation which came in hot at 1.9% which was a slight uptick of 1.8% from Q3. Inflation in Australia for the past 12 months is now 7.8% which is a 50 bps increase from 7.3%. I don’t need to tell you that prices are going up but regardless the result would’ve surprised the RBA considering that interest rates have increased at their fastest rate in history, going from 0.1% in April to 3.1% in December.

Australian Inflation Rate QoQ

Source: Trading Economics

Another critical data point is the unemployment rate. In December 2022, Australia maintained its very low rate of 3.5%. While this missed estimates of 3.4% and there are some worrying signs for the future, the fact remains that 13.75 million Australians are still employed, near an all-time high, and this will continue to add pricing pressure.

Other key points of data to note are:

- Business confidence in December increased from November but still remained negative, going from -4 to -1.

- MoM retail sales surprised with a decline 3.9% in December, likely due to Christmas spending brought forward to November black Friday sales. The result also flies in the face of trading updates from Myer, Super Retail Group, and JB Hi-Fi who all posted very strong increases in sales over the Christmas period.

- Building permits surged to 16,556 in December from 13,977 in November. The figures are still well below the highs of 2021 but a positive trend is forming.

The Case for Cutting Rates

There isn’t one and nobody in the market is expecting that to be a likely scenario.

The Case for Holding Rates

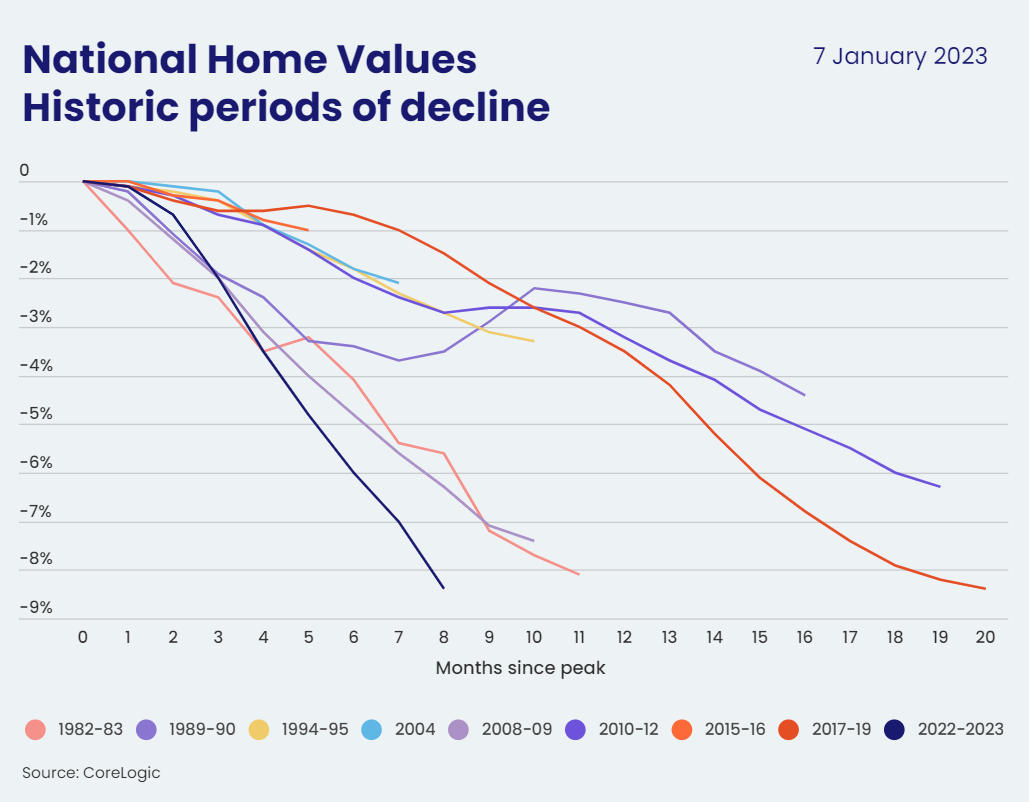

The arguments for holding rates aren’t strong and again most economists don’t believe this is a high probability scenario. However, one area of keen interest from the RBA will be housing prices which continue to fall at record rates. According to data from CoreLogic, their Home Value Index (HVI) has declined 8.9% from its peak in April 2022 right when interest rates started to increase. Given the “wealth effect” that is derived from Australians being extremely wealthy due to their housing assets, the RBA may give pause in order to provide a reprieve on this sector.

Source: CoreLogic

The Case for Raising Rates

By a country mile the most likely outcome but the divergence is on by the quantum. Those arguing for a 15 bps rise point to the negative housing data and the impending mortgage cliff of fixed-rate mortgages due to reprice by July. Last year the RBA commissioned a study to gain insight into the level of mortgage stress at various interest levels. It found that at 3.6%, more than half of homeowners would see a 20% decline in the cash they have available after paying their mortgage costs. A 15 bps increase would take rates to 3.25% and leave very few bullets in the chamber for the RBA.

The most likely outcome is a 25 bps hike due simply to the fact that the RBA doesn’t like to surprise the market too much. The data outlined above also supports this move. For the past three meetings the RBA has raised by 25 bps and while there are early signs that the rapid increase in rates is having the desired effect, the fact remains that inflation continues to increase which is why they will have no choice but to raise. I would say 50 bps isn’t off the table but unlikely given the arguments for a 15 bps hike or pausing. It would have a higher probability of a 15 bps hike in my opinion.

New Zealand Inflation Rate

Source: Trading Economics

New Zealand continues to be a good barometer for the RBA. They raised 75 bps in their last meeting, November 2022, to 4.25% before taking a two month vacation. While their housing market is also under pressure from high rates and overleveraged homeowners, the most recent inflation data shows that they will need to raise further, albeit at a slower rate in order to truly get inflation under control. The most recent data shows Q4 inflation decreasing from 2.2% in Q3 to 1.4%. However, the 12 month rate held steady at 7.2% and the current annualised rate is 5.6%, suggesting that they still have a way to go to tame the inflation monster. The same can be said for the RBA which is why the discussion for pausing rates is a bit premature at this stage.

We offer value-rich content to our BPC community of subscribers. If you're interested in the stock market, you will enjoy our exclusive mailing lists focused on all aspects of the market.

To receive our exclusive E-Newsletter, subscribe to 'As Barclay Sees It' now.