Every Tuesday afternoon we publish a collection of topics and give our expert opinion about the Equity Markets.

Last week all eyes were on the Bank of Japan (BoJ) as there was speculation that the last hold-out of ultra-easy monetary policy and quantitative easing (QE) would start to reverse course. Unfortunately the BoJ disappointed the market with no change made to interest rates or yield curve control (YCC). ABSI this week discusses the Japanese conundrum.

As a reminder, the BoJ currently sets interest rates at 0.1% and targets a 10y Japanese Government Bond (JGB) yield of 0% with a 0.5% band - meaning that if the yield rises above 0.5% then the BoJ will step in and purchase JGBs until the yield drops below 0.5%. The purpose of this loose monetary policy is to stimulate demand and inflation in an economy that has gone sideways for the last 30 years.

Recently, bond traders have tested the resolve of the BoJ by pushing on the 0.5% threshold and to-date the BoJ has stuck to its guns and kept the 10Y yield below the target. However, this defence has come at a great cost. All this QE has resulted in the BoJ owning approx. 53% of all JGBs outstanding. In January alone the BoJ spent over ¥1.4 trillion (A$15.5 billion) in purchasing JGBs. This has ballooned the BoJ’s balance sheet of JGBs to over ¥565.5 trillion (A$6.2 trillion) which is ~144% of GDP. If the BoJ keeps up this pace of buying, it will own 100% of the JGB market by the end of 2023.

Source: World Government Bonds

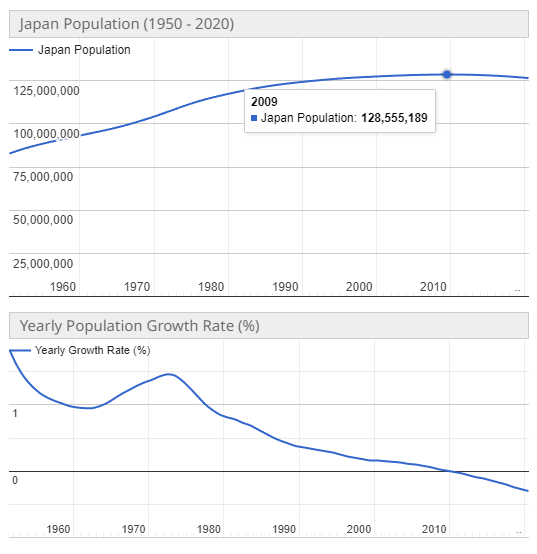

Taking a look back, it is difficult to discern the reason for the stagnation in the Japanese economy since the 1990’s. The reason most commonly cited is the country’s ageing population and low birth rate contributing to a population collapse. The Japanese population peaked in 2009 at ~128.5m and has since fallen back to just under 125.5m at the time of writing. Furthermore, Japan’s dependency ratio, which is the population over 65 as a share of working age population (15-64), is one of the highest in the OECD at 71.12% in 2021; an increase of ~10% in the last 10 years. Even more distressing is the Japanese birth rate down to 1.34 births per woman in 2020. As a result of these statistics, the UN forecasts the Japanese population to decline to ~73.6m by 2100.

Source: WorldOMeters

These worrying demographic statistics mean that tax revenues are lower and spending on welfare is rising resulting in ballooning government debt. Japan is the most indebted economy in the world, as a percentage of GDP, with usdebtclock.org estimating a public debt to GDP ratio of 296.1%

Source: usdebtclock.org

The quadrillion yen question is how is this all going to end? The honest answer from “experts” should be that we don’t know. But one thing is for sure, a country that continues to fiscally overspend and have its reserve bank purchase the debt to finance the spending will ultimately destroy its currency. Japanese economic leaders have been trying to spur inflation for over 30 years. I say, be careful what you wish for.

Video Transcript

One of the most important Bank of Japan interest rate meetings occurred last week, and the market was pricing in them changing tack and finally ending their loose monetary policy. Unfortunately, they defied market expectations and they maintained their negative interest rates and maintaining yield curve control of 0% on the Japanese tenure.

Now the market likes to test this resolve by selling Japanese government bonds into the market, which forces up the yield. This forces the Bank of Japan to purchase bonds to bring the yields back down, and as a result, in the 10 days in January, 1.4 trillion yen was spent by the Bank of Japan in order to maintain that yield, and that's ballooned their balance sheet to 565 trillion in Japanese government bonds.

They own over 50% of all Japanese bonds outstanding, which has all sorts of problems with how the market flows and fluctuates. This is leading to a lot of market participants leaving the Japanese government bond market, which is having disastrous effects on the yen. The Yen has depreciated significantly against all currencies, and there looks to be no sign of recovery unless the Bank of Japan changes tack and starts to ease off this loose monetary policy that they've held in place for almost 30 years.

To learn more, please subscribe to, as Barclay sees it, by clicking the link in the description.

We offer value-rich content to our BPC community of subscribers. If you're interested in the stock market, you will enjoy our exclusive mailing lists focused on all aspects of the market.

To receive our exclusive E-Newsletter, subscribe to 'As Barclay Sees It' now.