Every Tuesday afternoon we publish a collection of topics and give our expert opinion about the Equity Markets.

In a landmark move that could spell the end of checkout surcharges and reshape how Australians pay, the Reserve Bank of Australia (RBA) has released a consultation paper proposing a ban on credit and debit card surcharging. The central bank claims this would save shoppers up to $1.2 billion a year, marking the most significant overhaul of merchant payment rules in two decades. ABSI this week digs into how the payments infrastructure works in Australia and if a ban on surcharging will really save consumers.

It is important to appreciate that the proposal arrives at a time when cash is no longer king in Australia. In 2007, cash accounted for nearly 70% of all transactions. By 2022, that number had plummeted to just 13%, as tap-and-go, mobile wallets, and online checkouts replaced notes and coins. The convenience of cards and phones has come at a cost, as Australians swiped and tapped their way through a cashless economy, they also paid billions in hidden and not-so-hidden fees along the way.

Now, the RBA wants to simplify those costs, eliminate surcharges, and force the payments industry to absorb the burden. But behind the promise of a fairer system lies a complex web of fees, powerful stakeholders, and uncertainty on whether consumers will actually save.

To fully grasp the argument, it requires a basic understanding of the payments infrastructure in Australia. Every time you tap your card, whether it’s physical or through Apple Pay, a chain of events is triggered. Multiple parties are involved, each taking a cut of the transaction, forming what’s known as the card payment "rails".

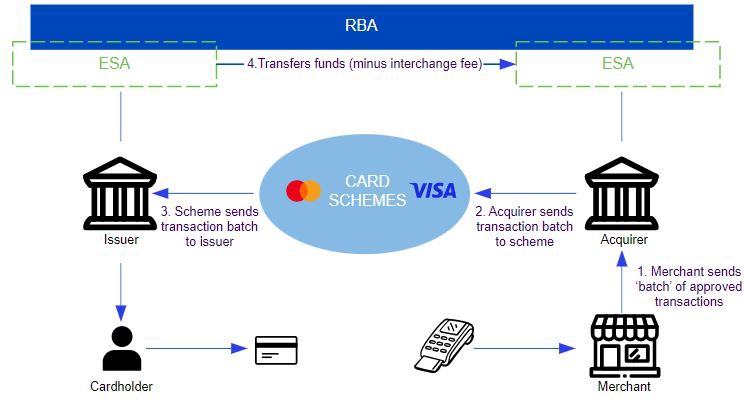

The Four-Party Model (Visa, Mastercard, eftpos)

Most debit and credit card payments in Australia use this open-loop, four-party system:

- Cardholder – You, the consumer.

- Issuer – Your bank, which issued your card (e.g. CBA, NAB).

- Acquirer – The merchant’s bank or payment service provider (e.g. Tyro, Square).

- Card Network – Visa, Mastercard, or eftpos, which routes and authorises the payment.

For a $100 transaction, here’s a simplified breakdown of who gets what:

- Interchange Fee: ~0.2%–0.8%, paid by the acquirer to the issuer (i.e. merchant’s bank pays your bank).

- Scheme Fees: Small but recurring fees paid by both acquirer and issuer to the card network.

- Acquirer Margin: A fee charged by the acquirer to the merchant, typically blended into a "merchant service fee" of 0.5–1.5%.

To recoup these costs, merchants often surcharge consumers 1% or more on credit, sometimes up to 3% for international cards.

Source: Lexology

And then there's Apple Pay.

If you’re using Apple Pay, there’s another player in the chain. Unlike Google Pay and Samsung Pay, which don’t charge banks, Apple takes a cut of every transaction, reportedly around 0.05%–0.15%. This charge is paid by the issuing bank, not the consumer directly. But banks can’t surcharge Apple Pay, and they can’t build competing wallets on iPhones due to Apple’s NFC restrictions. So, they absorb the cost, or find subtle ways to pass it on, such as scaling back on rewards or hiking interest rates. A major criticism of Apple is that it is effectively enacting an extra toll on the payments network without contributing to its operation and stability. As a result, it is reported that major banks are considering pulling out of Apple Pay, branding it a high-cost channel that offers little visibility and control.

The RBA’s consultation report, released in July 2025, proposes a bold three-pronged reform:

- Ban Card Surcharges:

- Remove the current prohibition on “no-surcharge” rules.

- This would allow card networks to reimpose their old no-surcharge rules, effectively banning surcharging for all Visa, Mastercard, and eftpos transactions.

- Lower Interchange Fee Caps:

- Reduce the domestic interchange caps, which would especially help small merchants who currently pay close to the cap.

- Introduce new caps for foreign-issued cards, currently unregulated and often the most expensive.

- Boost Pricing Transparency:

- Require banks and payment service providers (PSPs) to clearly disclose merchant fees.

- Force card networks to publish their wholesale fees and justify any increases.

The winners from this proposal will be consumers being surcharged on card purchases, 90% of merchants who don’t charge a card surcharge, and PSPs offering low-cost plans. The losers will be banks and card issuers currently making ~$900m in interchange revenue, large merchants who leverage their scale to negotiate better rates, and rewards programs, most notably Qantas Frequent Flyer, who are paid from interchange fees to provide points.

Noteworthy, one major player not bound by the same rules is American Express.

Source: BPC, OpenAI

Amex operates a closed-loop system: it is the issuer, the network, and the acquirer. This three-party model allows it to bypass the regulated interchange structure entirely enabling higher merchant fees which are funnelled into generous rewards programs. Crucially, it is not subject to the RBA’s interchange caps, so Amex could gain a competitive edge if Visa and Mastercard fees are suppressed.

Here’s the billion-dollar question: Will the average shopper actually see the $1.2 billion windfall promised by the RBA?

Possibly, but not in the way they expect. If merchants can’t surcharge, many will bake the cost of card payments into their prices. For businesses already doing that, not much changes. But for low-margin industries or merchants that rely heavily on surcharges, prices may rise quietly.

The RBA’s proposal is a bold attempt to modernise a system that’s evolved in complexity and opacity. Whether it leads to genuine savings or just a rebalancing of the same costs remains to be seen. What’s clear is that the age of the checkout surcharge may soon be over and with it, the golden era of rewards cards may be fading, too.

We offer value-rich content to our BPC community of subscribers. If you're interested in the stock market, you will enjoy our exclusive mailing lists focused on all aspects of the market.

To receive our exclusive E-Newsletter, subscribe to 'As Barclay Sees It' now.

{kind=link}